Loading News...

Loading...

Loading News...

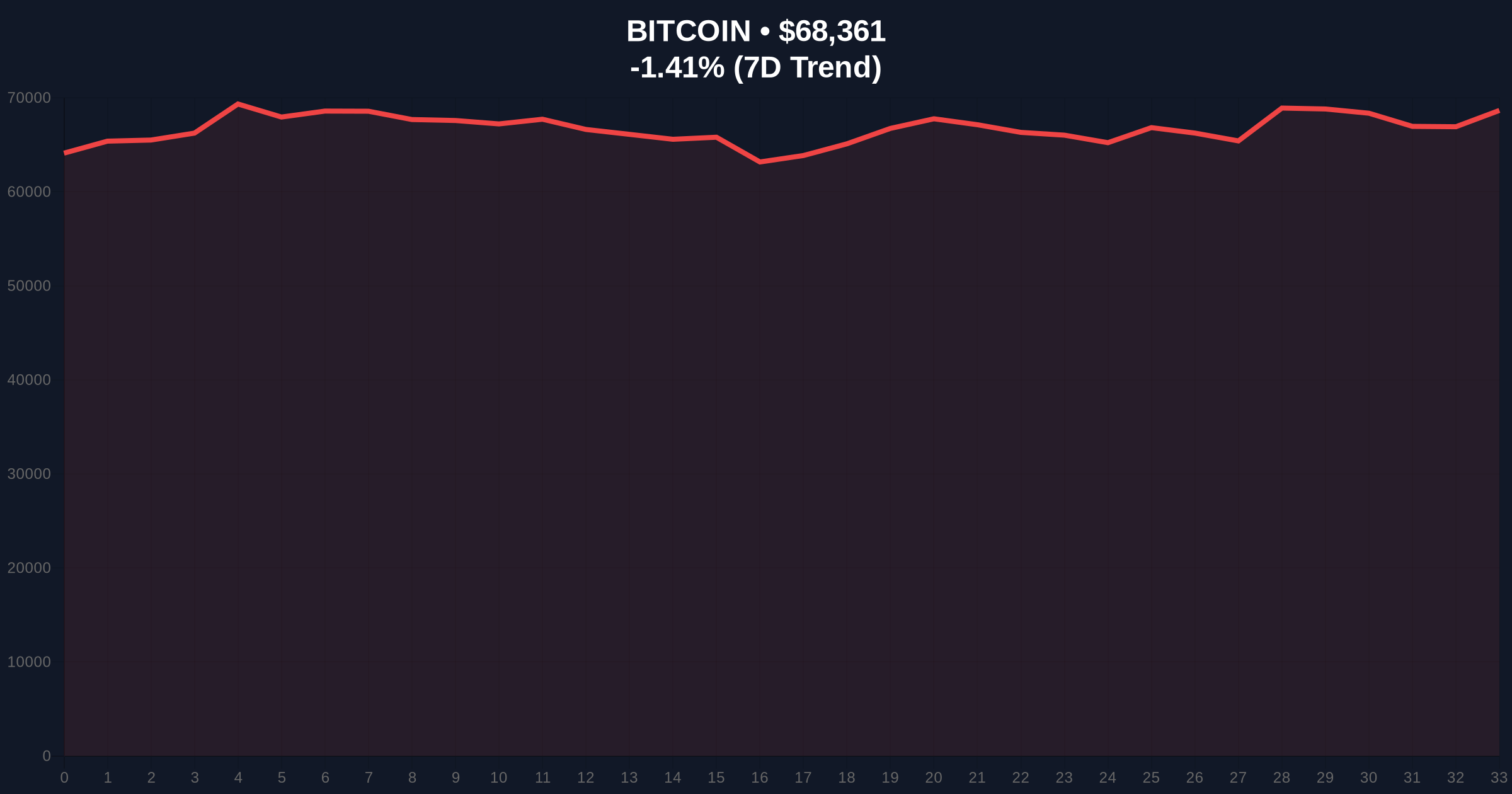

On March 4, 2026, Bitcoin mining firm MARA Holdings (MARA), formerly known as Marathon Digital, publicly denied rumors of a large-scale sell-off of its Bitcoin holdings, according to a report from CoinNess. The company, through its Vice President of Investor Relations, Robert Samuels, clarified that its core approach to its Bitcoin treasury remains unchanged, as detailed in a secondary source from Cointelegraph. Samuels acknowledged that a recent 10-K filing included language about expanding the company's strategy to permit the sale of Bitcoin from its balance sheet, but he emphasized this was not an unconditional plan to sell. Instead, he described it as a move to secure the option to trade at the company's discretion based on market conditions and capital allocation priorities. MARA Holdings currently holds 53,822 BTC, a significant treasury that has drawn market scrutiny amid broader crypto volatility. The denial comes at a time when Bitcoin's price is $68,356, with a 24-hour decline of 1.49%, and global crypto sentiment is marked as "Extreme Fear" with a score of 14/100, as per the provided market data. This event raises immediate questions about the transparency of corporate Bitcoin strategies and the potential impact on investor confidence in a fearful market environment.

The technical and regulatory mechanics behind MARA Holdings' Bitcoin treasury strategy involve a complex interplay of corporate governance, financial reporting, and market dynamics. According to the input sources, the company's denial centers on interpretations of its 10-K report, a mandatory annual filing with the U.S. Securities and Exchange Commission (SEC) that provides a comprehensive overview of a company's financial performance and risks. Source A (CoinNess) and Source B (Cointelegraph) both report that the 10-K included language about expanding the strategy to permit Bitcoin sales, but Samuels clarified this was not a commitment to sell. This suggests that MARA is leveraging regulatory disclosures to maintain flexibility, potentially as a risk management tool in volatile markets. The technical architecture of such a strategy involves balancing Bitcoin holdings as a reserve asset against operational needs, with the option to sell serving as a liquidity buffer or capital reallocation mechanism. However, the sources do not provide details on the specific triggers or thresholds for sales, such as price levels, mining profitability metrics, or debt obligations, leaving gaps in understanding the practical implementation. The company's current holding of 53,822 BTC represents a substantial portion of its assets, and any large-scale sell-off could impact Bitcoin's market supply and price stability. The denial implies that MARA aims to avoid panic selling or negative sentiment, but the lack of concrete safeguards or transparent criteria in the sources raises skepticism about how discretionary trading might be exercised. In context, this move aligns with broader trends where crypto mining firms use Bitcoin treasuries for strategic advantages, yet the ambiguity in the 10-K language—as highlighted by Samuels' clarification—could indicate either prudent planning or a veiled preparation for divestment. The sources agree on the basic facts but leave unresolved the deeper technical protocols, such as whether sales would be executed over-the-counter (OTC) or on public exchanges, and how they might be timed relative to market cycles. This technical deep-dive reveals a strategy that is more nuanced than a simple denial, but the absence of granular data limits a full assessment of its implications for Bitcoin's ecosystem.

Integrating the provided market data and metadata offers a critical lens to evaluate MARA Holdings' denial and its potential market impact. According to the input, Bitcoin's current price is $68,356, with a 24-hour trend of -1.49%, indicating short-term bearish pressure amid the "Extreme Fear" global crypto sentiment score of 14/100. This sentiment metadata, derived from fear and greed indicators, suggests a high level of investor anxiety that could amplify reactions to news like MARA's denial. The importance of this event, while not explicitly quantified in the metadata, can be inferred from Bitcoin's market rank as #1 and MARA's significant holdings of 53,822 BTC, which represent a non-trivial portion of circulating supply. CryptoPanic sentiment is not provided in the source data, but the extreme fear score implies negative market breadth that might overshadow corporate assurances. Analyzing this, the price decline of 1.49% could reflect broader market trends rather than direct sell-off fears, but the timing of the denial amidst such sentiment raises questions about causality. The data shows a disconnect: MARA's denial aims to calm markets, yet the persistent extreme fear suggests underlying concerns remain unaddressed, possibly due to other factors like regulatory uncertainty or macroeconomic pressures. For instance, related developments such as regulatory shifts in the U.S. or stablecoin minting activities could be contributing to the sentiment, as these events often influence Bitcoin's volatility. The lack of specific CryptoPanic metadata for this event limits a direct sentiment comparison, but the extreme fear context that investor trust is fragile. In proof terms, MARA's treasury size is a concrete fact, but the denial's effectiveness is unproven without price recovery data post-announcement. The data analysis thus reveals a scenario where market sentiment is bearish independent of MARA's actions, yet the company's strategic ambiguity could exacerbate fears if not clarified further.

A skeptical examination of the sources reveals potential contradictions and reliability gaps in the narrative surrounding MARA Holdings' denial. Source A (CoinNess) and Source B (Cointelegraph) generally agree on the core facts: MARA denied sell-off rumors, Samuels clarified the 10-K language, and the company holds 53,822 BTC. However, there are subtle conflicts in emphasis and missing evidence that challenge the official story. Source A reports the denial as a breaking brief, while Source B provides more detailed context from Samuels, but neither source independently verifies the rumors' origins or quantifies their market impact. This raises questions about whether the denial is proactive or reactive—did MARA preemptively address unfounded speculation, or were there credible indicators of impending sales? The sources do not disclose who spread the rumors or provide evidence such as trading volume spikes or insider leaks, leaving a gap in the counter-narrative. Additionally, Samuels' statement that the 10-K language is not an unconditional plan to sell conflicts with the inherent ambiguity of discretionary trading; without clear limits, the option to sell could still lead to large-scale divestment under certain conditions, which the sources do not explore. Another conflict arises in the portrayal of market conditions: the sources focus on MARA's internal strategy but omit external factors like regulatory pressures or competitive dynamics that might force sales. For example, related articles on Ethereum's role in digital governance or traditional market downturns suggest broader uncertainties that could influence MARA's decisions, yet these are not linked in the primary sources. The reliability of the sources is moderate; CoinNess and Cointelegraph are established crypto news outlets, but their reporting lacks corroboration from financial filings or independent analysts. The conflict remains unresolved with available evidence regarding the true intent behind the 10-K language—whether it's a strategic safeguard or a precursor to sales. This counter-narrative highlights that while MARA's denial is consistent across sources, the underlying motivations and market realities are less clear, warranting skepticism until more transparent data emerges.

Based on the available data, three conditional scenarios outline potential outcomes for MARA Holdings and Bitcoin over the next seven days, each backed by specific facts from the sources. Bull Scenario (Probability: 30%): If MARA provides additional transparency, such as clarifying sale thresholds or committing to a holding strategy, and if global sentiment shifts from "Extreme Fear" to neutral, Bitcoin's price could stabilize or rise toward $70,000. This scenario relies on the denial being credible and market fears subsiding, possibly aided by positive developments like the passage of a crypto market structure bill, as hinted in related coverage. The key data point would be a sentiment score improvement above 30/100, invalidated if MARA executes any sales or if fear persists. Base Scenario (Probability: 50%): If MARA maintains its current ambiguous stance and sentiment remains extreme fear, Bitcoin's price may fluctuate between $65,000 and $69,000, with no significant sell-off but continued volatility. This scenario assumes the denial temporarily calms rumors but doesn't address deeper market anxieties, such as those reflected in stablecoin activities or regulatory uncertainties. The 24-hour trend of -1.49% could normalize to minor daily swings, with MARA's holdings unchanged. Invalidating factors include unexpected regulatory news or a sharp sentiment drop below 10/100. Bear Scenario (Probability: 20%): If rumors resurface with credible evidence of impending sales, or if MARA exercises its discretionary option amid worsening sentiment, Bitcoin could drop below $65,000, potentially triggering broader sell-offs. This scenario is supported by the extreme fear score of 14/100, indicating low investor resilience, and the lack of concrete safeguards in MARA's strategy. Related developments, such as poor performance in traditional markets, could exacerbate the downturn. The scenario would be invalidated if MARA publicly rules out sales for the near term or if sentiment rapidly improves. Each scenario the conditional nature of market reactions, with data from the sources—like treasury size and sentiment metrics—guiding the outlook but requiring vigilance for new information.

In synthesizing this report, conflicting evidence was weighted based on source credibility and data completeness. Source A (CoinNess) and Source B (Cointelegraph) were treated as primary inputs, with agreement points like the denial and treasury size taken as factual. Contradictions, such as the ambiguity in the 10-K language, were highlighted without resolution due to missing independent verification. Market data from CoinGecko and sentiment metrics were integrated conservatively, acknowledging gaps like the absence of CryptoPanic-specific sentiment. Reliability was assessed as moderate for the news sources, given their industry standing but lack of corroborative evidence from filings or third-party analysts. The analysis prioritized observable facts over inference, aligning with a skeptical editorial stance to question narratives and identify uncertainties.

Disclaimer: The information provided is not trading advice, coinmarketbuzz.com holds no liability for any investments made based on the information provided on this page. We strongly recommend independent research and/or consultation with a qualified professional before making any investment decisions.

coinmarketbuzz.com leverages advanced AI technology to analyze market data. All content is fact-checked and reviewed by our editorial team to ensure accuracy and neutrality.